The Case Against Marathon Digital (MARA)

Thoughts on 13Mar2024

Investing is a marathon, not a sprint. - Common Sense

Intro:

Typically I don’t write a case against, but I would be remised not to give alternative perspectives here and there. Contrary to popular belief, not all stonks, only go up. This will be short and sweet. Let’s get into it.

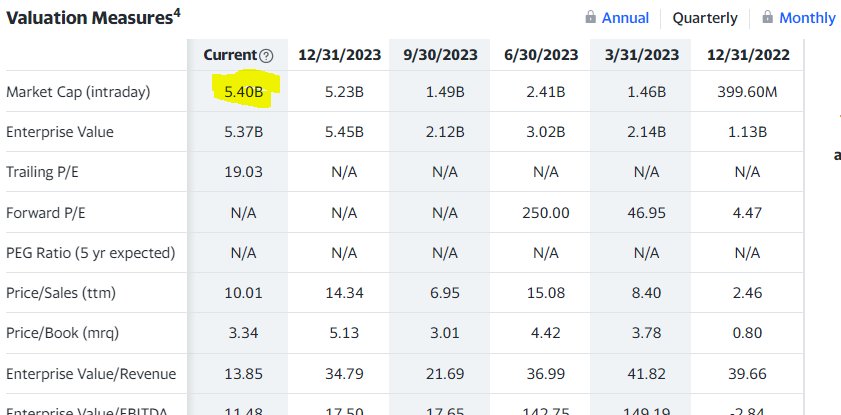

Valuation Discrepancies:

The first and main issue for me is that MARA BTC holdings value is only 1.5B as of 3/5/24. However, their MC, below is nearly 4x that value. Intrinsically, what else does MARA offer would be the first question to ask yourself, other than mining more future BTC? Does that make this valuation make sense? To me, no.

Dilution:

3/4/24 - 15M shares, 30M on aggragate (10% of OS shares) - this will continue, they will sell BTC or dilute to pay for energy and CAPEX. Share offering will only delay more dilution later. This is not a sustainable model for shareholders.

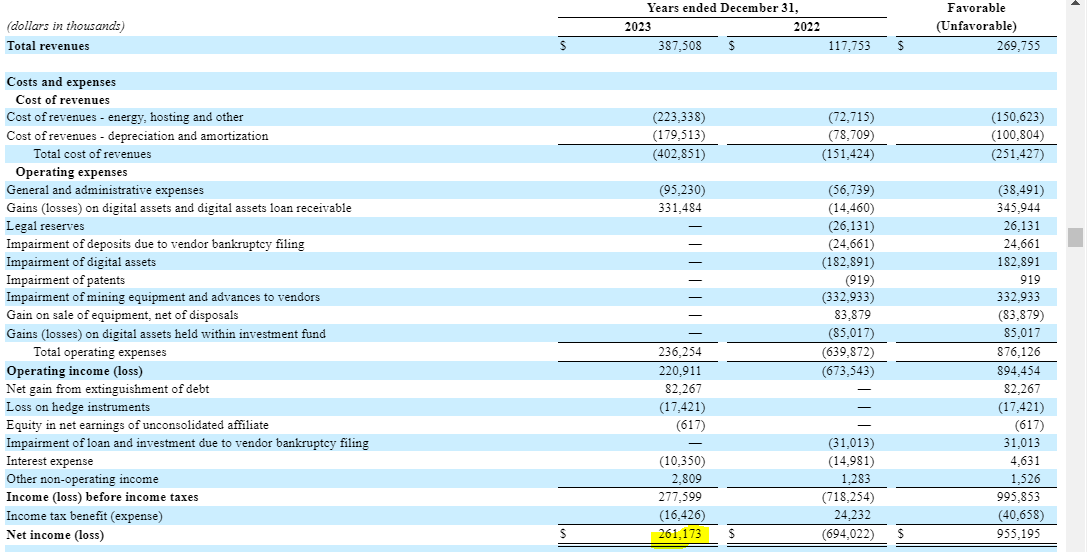

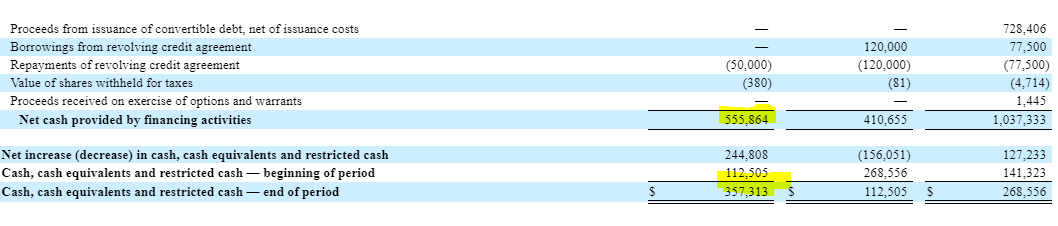

Finances:

To further the point above, MARA raised 555m in financing but only have 357m in cash at end of period FY23 - so they spent 200m on the year meaning they have decent runway but will need to sell BTC or finance again later down the road.

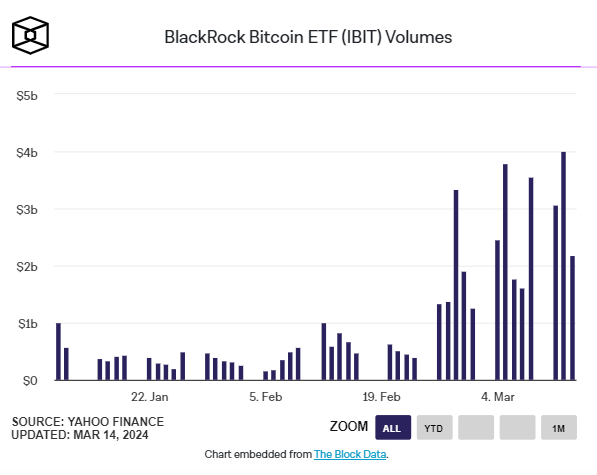

ETF Headwinds:

Inflows are now going into ETFs and BTC itself rather than miners. This is being seen across the board. Taking HUT for example, it is currently trading at a MC level with its BTC holding value. This makes more sense, but I still don’t like the business model and more folks will move to these ETFs rather than miners to get into the crypto space. Especically for BTC itself.

Using Black Rocks ETF (IBIT) for example. You can see the period of increasing inflows correlates to decreasing miner market caps. The transisition is clear. BTC price is moving up while miner values are moving down.

Conclusion:

In summary, miners like MARA have an unsustainable business model from the shareholder perspective at least. You’re buying it for BTC, which is no longer needed since ETFs now offer exposure outside of BTC itself. Continued selling to support their operations via dilution or BTC disposal will continue to put downward pressure on the stock. Note, Capex will only get worse with the halving, it will take more power and energy to mine even less BTC, Processing Units are not cheap…..This along with the risk that BTC value could also drop and a MC valuation that is 4x higher than their BTC holding is very unattractive. Disclosure: I am 610 shares short MARA at $19.85. I will look to exit when its closer to its BTC and Cash holding value which would put the stock around $6.

Please hit the “like” button above if you enjoyed reading the article, thank you. You can also see all of my trades at: https://thetagang.com/mehmehmeh